Own AED 2 million (roughly USD 545,000) worth of UAE real estate, and you can secure a renewable 10-year residency visa — no employer, no business licence, no local sponsor required. That, in one sentence, is why the UAE Golden Visa through property has become the most popular residency-by-investment route in the region.

And 2026 has made it dramatically more accessible. A federal policy circular issued in February 2026 removed the long-standing 50% down-payment requirement for mortgaged properties. Eligibility now rests on a single test: does your property — or combined portfolio — meet or exceed AED 2 million in Dubai Land Department (DLD) valuation? If yes, you can apply, whether the property is mortgaged, off-plan, or fully paid.

This guide explains exactly how the AED 2M rule works in 2026: what counts toward the threshold, what changed this year, where you can buy, the step-by-step application process, the full cost picture beyond the property itself, and honest answers to the questions investors ask most.

1. What Is the UAE Golden Visa Property Route?

The UAE Golden Visa is a long-term residence permit introduced in 2019 to attract investors, entrepreneurs, and skilled professionals. The real estate investor category grants a 10-year renewable visa to anyone who owns qualifying property worth at least AED 2 million.

What makes the property route stand out among the various Golden Visa categories is its independence. It is the only category that gives you a renewable ten-year permit without requiring you to maintain employment or active business operations in the Emirates. Buy the property, keep the property, keep the visa.

The headline benefits of the 10-year golden visa UAE property route:

-

● No stay requirement: You can remain outside the UAE for more than 180 days without losing your residency status — unlike standard residence visas, which lapse.

-

● Full family sponsorship: Sponsor your spouse, children (with no age cap for unmarried children in most cases), parents, and household staff.

-

● No sponsor or employer needed: Your property is your sponsor.

-

● Renewable: As long as you hold the qualifying property, the visa renews for further 10-year term.

-

● Stability for planning: A decade-long horizon for schooling, banking, business setup, and tax residency planning.

Other routes exist — business investors, specialised professionals, retirees with the 5-year retirement visa, and the 2-year property visa at lower thresholds — but for pure simplicity and duration, the AED 2M property route is the benchmark against which the others are measured.

2. The AED 2M Rule: Exactly What Counts

The AED 2 million threshold sounds simple, but the details determine whether your application sails through or gets rejected. Here is precisely how the rule works in 2026.

How the AED 2 Million Is Measured

Eligibility is assessed on the property value recorded with the Dubai Land Department — specifically, the purchase value on your title deed, supported by a DLD valuation certificate confirming the property meets or exceeds AED 2 million. It is not based on your down payment, your mortgage balance, or what a portal listing says your home is worth today.

Two important flexibilities:

- ● Multiple properties can be combined. You do not need a single AED 2M asset. Two apartments worth AED 1.1M and AED 950K, both registered in your name, can together satisfy the threshold.

-

● The valuation certificate is the arbiter. If you bought below AED 2M but the DLD valuation now certifies the property at or above AED 2M, speak to a specialist — valuation-based qualification has been accepted in many cases, though the safest route remains a purchase value at or above the threshold.

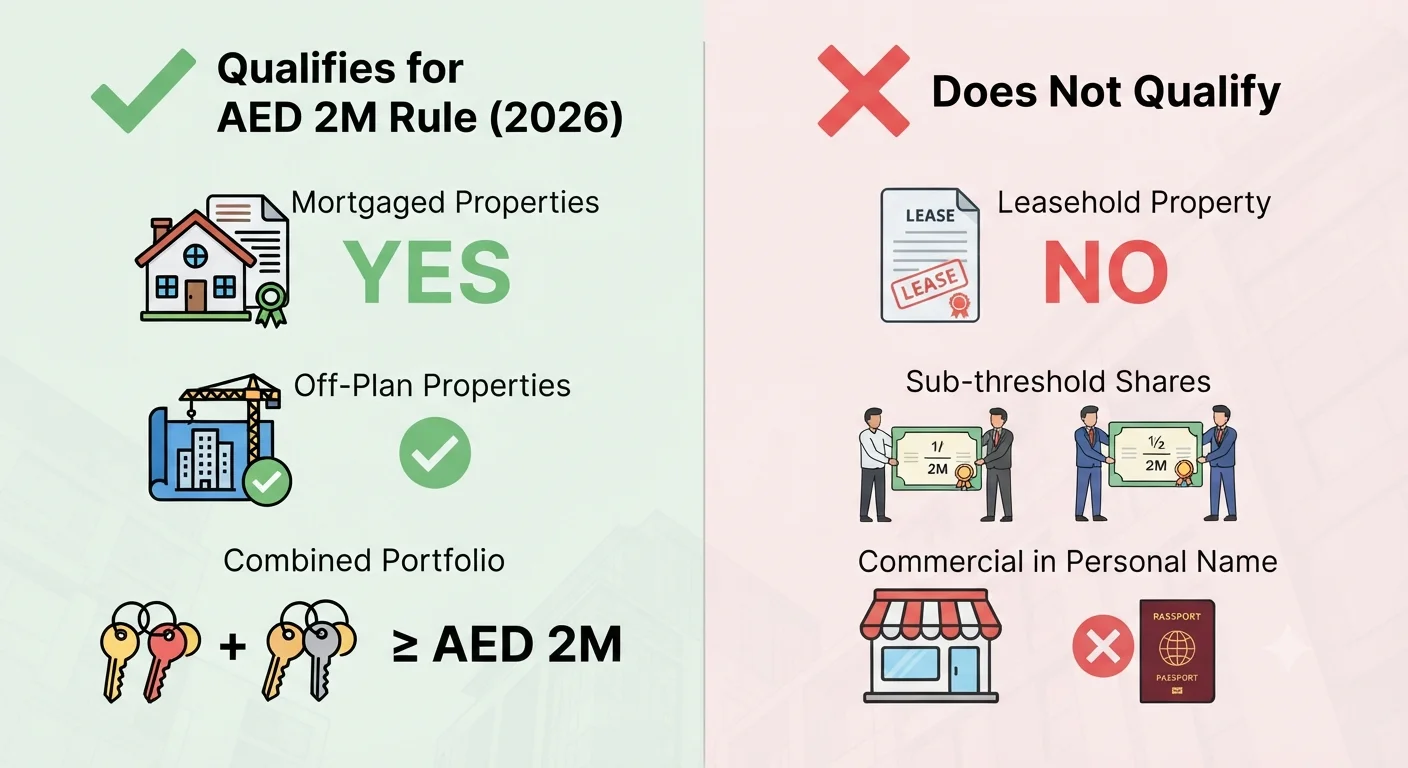

Mortgaged Property: The Big 2026 Change

This is the most significant update of the year. Until early 2026, applicants with mortgaged properties had to show they had paid at least 50% of the property value, or a minimum of AED 1 million, and provide a bank no-objection certificate (NOC).

The February 2026 federal circular removed the down-payment requirement entirely. Applications are now assessed solely on the DLD valuation certificate confirming the property meets or exceeds AED 2 million — regardless of how much of the mortgage you have paid off.

In practical terms: you could purchase an AED 2.2M apartment with a 20% deposit and a bank mortgage on the remainder, and qualify for the golden visa with mortgaged property from day one. Banks still issue an NOC as part of the process, and we recommend requesting it early — some DLD service centres continue to ask for it as supporting documentation.

Off-Plan Property: Yes, It Qualifies

Golden visa off-plan property purchases qualify, provided the unit is bought from a government-approved developer. A final title deed does not need to be issued at the time of application for approved off-plan units — the initial contract of sale (Oqood registration in Dubai) evidences your ownership.

Off-plan is often the most capital-efficient way to reach the threshold: you can combine multiple off-plan units to hit AED 2M, and payment plans spread the outlay. Browse current off-plan projects in the UAE to see qualifying inventory from approved developers such as Emaar, Sobha, Aldar, and Nakheel.

Joint Ownership and Spouses

Here is the misconception that catches out more applicants than any other: joint owners do not automatically qualify just because the total property value exceeds AED 2 million.

The rule is that each applicant's individual share must independently meet AED 2 million in DLD valuation. If you and a business partner own an AED 3M villa 50/50, neither of you qualifies — each share is worth only AED 1.5M.

For married couples, the position has been more generous in practice: spouses jointly owning a property have been able to qualify with an attested marriage certificate, with one spouse applying as the investor. Rules in this area have been clarified several times, so verify the current DLD position for your specific ownership structure before purchasing.

What Doesn't Qualify

-

● Leasehold property — the visa requires freehold ownership.

-

● Property outside designated freehold/investment zones.

-

● Shares in property below the threshold — as above, your individual share must reach AED 2M.

-

● Commercial structures held via certain company vehicles — ownership generally must be in your personal name (or specific approved holding structures); take advice before buying through a company.

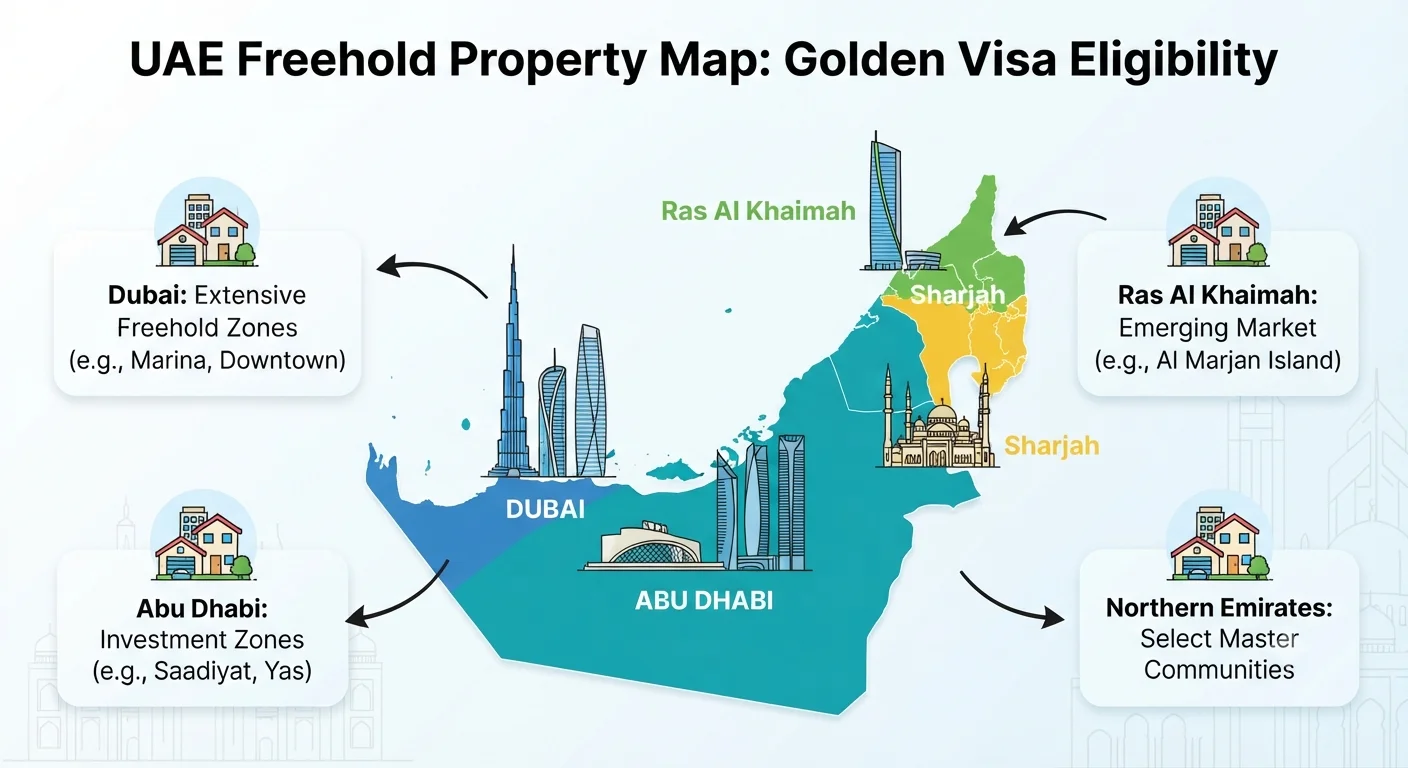

3. Where You Can Buy: Freehold Areas Across the UAE

The property must sit in a designated freehold area where foreign nationals can hold full ownership. This is where most guides stop at Dubai — but qualifying freehold property exists across the Emirates, and prices per square foot vary enormously between them.

Dubai offers more than 60 freehold zones, including Downtown Dubai, Dubai Marina, Palm Jumeirah, Business Bay, Jumeirah Village Circle (JVC), Dubai Hills Estate, and Mohammed Bin Rashid City. Explore off-plan projects in Dubai or properties for sale in the UAE to compare qualifying options.

Abu Dhabi grants freehold ownership to foreigners in investment zones such as Saadiyat Island, Yas Island, Al Reem Island, and Al Raha Beach. Premium waterfront communities from developers like Aldar make it straightforward to reach AED 2M with a single unit — see current Abu Dhabi off-plan developments.

Ras Al Khaimah is the value play of 2026. With the Wynn resort development driving appreciation on Al Marjan Island, Ras Al Khaimah investment properties offer waterfront product at prices well below comparable Dubai stock — while still qualifying for the golden visa when the threshold is met.

Sharjah and the northern emirates offer foreign ownership in specific master communities, though some operate on long-term usufruct rather than full freehold — check the tenure carefully, as leasehold and usufruct arrangements generally do not qualify.

For most investors the decision comes down to yield versus entry price: an AED 2M budget buys a one-bedroom in prime Dubai Marina, a two-bedroom in JVC or Dubai Hills, or a substantial waterfront residence in Ras Al Khaimah.

4. Step-by-Step: How to Apply in 2026

The process for a Dubai golden visa property application runs primarily through the Dubai Land Department; other emirates route through the Federal Authority for Identity, Citizenship, Customs and Port Security (ICP).

-

● Confirm your property qualifies. Check that the title-deed value (or combined values) meets AED 2 million and the property sits in a freehold zone. Obtain the DLD valuation certificate — this is the document the application turns on.

-

● Gather your documents. Title deed(s) or Oqood for off-plan, passport (6+ months validity), passport photo against a white background, valid UAE health insurance, your current visa or entry permit, and the bank NOC if the property is mortgaged.

-

● Submit the application. In Dubai, apply digitally through the DLD Cube platform or in person at a DLD service centre. The DLD coordinates with the immigration authority (GDRFA) on your behalf.

-

● Complete medical and biometrics. A standard medical fitness test (blood test and chest X-ray) plus Emirates ID biometrics.

-

● Receive approval and your 10-year visa. Once issued, you can add dependants — spouse, children, parents, and household staff — under your sponsorship.

Typical timeline: most straightforward applications complete within two to four weeks of the valuation certificate being issued. Complications — joint ownership structures, off-plan documentation gaps, missing NOCs — are what cause delays, which is why pre-checking eligibility before you buy matters.

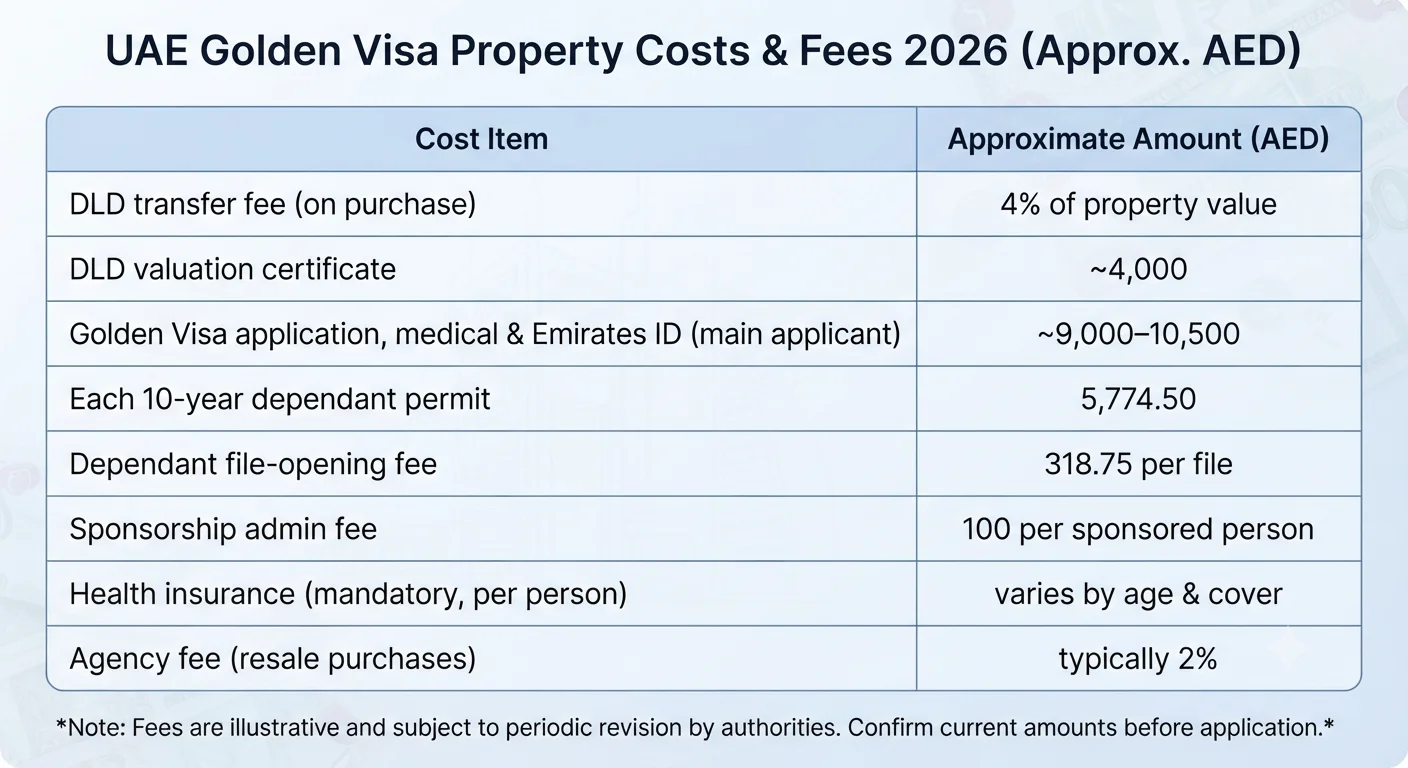

5. Costs Beyond the AED 2M

Budget for meaningful costs on top of the property price itself. Approximate 2026 figures for a Dubai application:

|

Item |

Approximate Cost (AED) |

|

DLD transfer fee (on purchase) |

4% of property value |

|

DLD valuation certificate |

~4,000 |

|

Golden Visa application, medical & Emirates ID (main applicant) |

~9,000–10,500 |

|

Each 10-year dependant permit |

5,774.50 |

|

Dependant file-opening fee |

318.75 per file |

|

Sponsorship admin fee |

100 per sponsored person |

|

Health insurance (mandatory, per person) |

varies by age & cover |

|

Agency fee (resale purchases) |

typically 2% |

So a family of four should allow roughly AED 30,000–40,000 in visa-related costs on top of the property transaction — modest relative to the AED 2M investment, but worth planning for. Fees are revised periodically; confirm current amounts with the DLD before applying.

6. Is the AED 2M Property Route Worth It? An Investor's View

The honest answer: for most buyers who want UAE residency anyway, yes — because the visa comes attached to an asset that works for you.

The case for it. Gross rental yields in qualifying communities typically run 5–8% — JVC, Dubai Sports City, and parts of Ras Al Khaimah at the higher end; prime Palm Jumeirah and Downtown at the lower end but with stronger capital-appreciation history. Compare that with residency-by-investment programmes elsewhere that require donations or near-zero-yield government bonds, and the UAE proposition is unusually productive: your qualifying asset pays rent. Add zero income tax, no annual property tax, and the security of residency that doesn't evaporate if you change jobs, and the appeal is clear.

The risks, stated plainly. UAE property is cyclical — values fell meaningfully between 2014 and 2020 before the current boom, and buyers at 2026 prices should underwrite conservatively. Off-plan carries completion risk; buying from established, government-approved developers mitigates but does not eliminate it. And visa rules change: the down-payment rule was removed in 2026, but thresholds and conditions have been adjusted before (the threshold itself survived the April 2026 rule revisions) and could be again. Your visa also depends on retaining the qualifying property — sell below the threshold and the residency basis falls away at renewal.

If the property purchase makes sense on its own merits, the Golden Visa is an exceptional bonus. If the visa is the only reason to buy, be more careful — and buy quality in proven locations.

7. FAQ

Can I get a Golden Visa with a mortgaged property in 2026?

Yes. The February 2026 federal circular removed the previous 50% down-payment (minimum AED 1M) requirement. Eligibility is now based solely on the property meeting AED 2 million in DLD valuation, regardless of mortgage status. Obtain a no-objection certificate from your lender to support the application.

Does off-plan property qualify for the UAE Golden Visa?

Yes, if purchased from a government-approved developer. A final title deed is not required at application for approved off-plan units — the registered initial contract of sale (Oqood) evidences ownership.

Can I combine two or more properties to reach AED 2 million?

Yes. Multiple properties registered in your name can be combined to satisfy the threshold, including a mix of ready and off-plan units.

Do joint owners or spouses both get the visa?

Each applicant's individual share must independently meet AED 2 million. Married couples jointly owning a property have been treated more flexibly with an attested marriage certificate, but verify the current DLD position for your structure before buying.

Is the AED 2M based on purchase price or current market value?

The purchase value recorded on the title deed, supported by a DLD valuation certificate. Current portal estimates are irrelevant; the DLD's figures govern.

What happens if I sell the property?

Your visa is tied to holding qualifying property. If you sell and drop below AED 2M in registered holdings, you lose the basis for the visa — typically at renewal, though you should take advice on your specific position before selling.

Can I sponsor my parents on a property Golden Visa?

Yes. Golden Visa holders can sponsor spouses, children, parents, and household staff for the duration of the visa.

How long does the application take?

Most clean applications complete within two to four weeks of the DLD valuation certificate being issued.

8. Conclusion: The Simplest Path to a Decade in the UAE

The AED 2M rule in 2026 is more accessible than it has ever been: one threshold, assessed on DLD valuation, with mortgaged and off-plan property fully in scope and the old down-payment barrier gone. Buy AED 2 million of freehold property in the right zone, and a renewable 10-year residency — with full family sponsorship and no minimum stay — follows.

The variables that decide whether your application succeeds are set before you buy: freehold tenure, approved developer, ownership structure, and title-deed value. That is where specialist guidance pays for itself.

FP Property tracks Golden Visa-eligible inventory across all seven emirates — ready and off-plan, from AED 2M single units to combined portfolios. Speak to our Golden Visa property specialists for a tailored shortlist of qualifying properties, or start browsing properties for sale in the UAE today.