Why Credit Score Is More Important Than Ever in the UAE Mortgage Market?

Buying a home in the UAE used to rely primarily on income, job security and current debts. Today, credit scores are at the centre of nearly any mortgage decision. Banks now have stricter rules for lending, and they use strict data to judge the financial behaviour of a borrower. This shift occurred because the mortgage market has matured. Banks like to reduce risk, and buyers want more lending rules to be transparent.

The Al Etihad Credit Bureau (AECB) plays a major role in this new landscape. The bureau gathers financial information from banks, telecommunications companies and other institutions. Then it generates a credit report and score for every resident and citizen. Banks, because the system is unified, trust the information and use it heavily in deciding whether to approve a mortgage or not.

In short, your score affects your chances of approval, the amount of loan you will receive, the rate of interest you will incur and even the kind of mortgage you will be eligible for. Understanding the working of the system helps you to prepare smarter and avoid any surprises in the future.

What is a UAE Credit Score? (AECB Score Explained Clearly)

A UAE credit score is generated by AECB. The bureau functions in the role of a national credit data authority. Every financial activity that involves repayment, borrowing or missed payments is tracked. AECB takes this information and uses it to produce a score ranging from 300 to 900.

The score indicates how reliable a borrower you are. A low score will generally mean late payments, bounced cheques or large outstanding debts. A high score indicates good repayment habits and low risk.

These things affect your UAE credit score:

- ● Number of loans or credit cards you already have

- ● Your repayment consistency

- ● How much of your credit limit is occupied

- ● Bounced cheques

- ● Recent credit applications

- ● Length of your credit history

- ● Credit mix — having a healthy variety of loans, credit cards and mortgages also positively influences your score

Most banks require a minimum credit score of 700 or above for mortgage approval, with scores above 700 considered ideal for streamlined approval and access to better interest rates. A score of 650 to 699 is still considered by many banks, but the terms may not be the best available in the market.

How UAE Banks Use Credit Scores in Mortgage Decisions

When lenders review a mortgage application, the first step they take is to check the AECB credit score. But banks do not depend only on the score. They go much deeper.

Here is what lenders tend to look for:

- ● Payment history (loans and credit cards)

- ● Frequency of late or missed payments

- ● Bounced cheques in the last few years

- ● Number of open credit facilities

- ● Overall credit exposure

- ● Changes in outstanding balances

- ● Credit utilisation patterns

- ● Stability of income

Most banks require a minimum credit score of 650 for mortgage eligibility. However, a score of 700–720 or higher is considered ideal, as it streamlines the approval process and significantly improves the chances of securing more favourable interest rates.

Your credit score affects:

- ● Mortgage eligibility

- ● Maximum loan amount

- ● Required down payment

- ● Interest rate

- ● Speed of approval

Mortgage brokers also check your credit score when pre-approving you. They read through the report to determine potential issues before they pass your application through to a bank. This early review is a way of avoiding unnecessary declines — which will reduce your score even further.

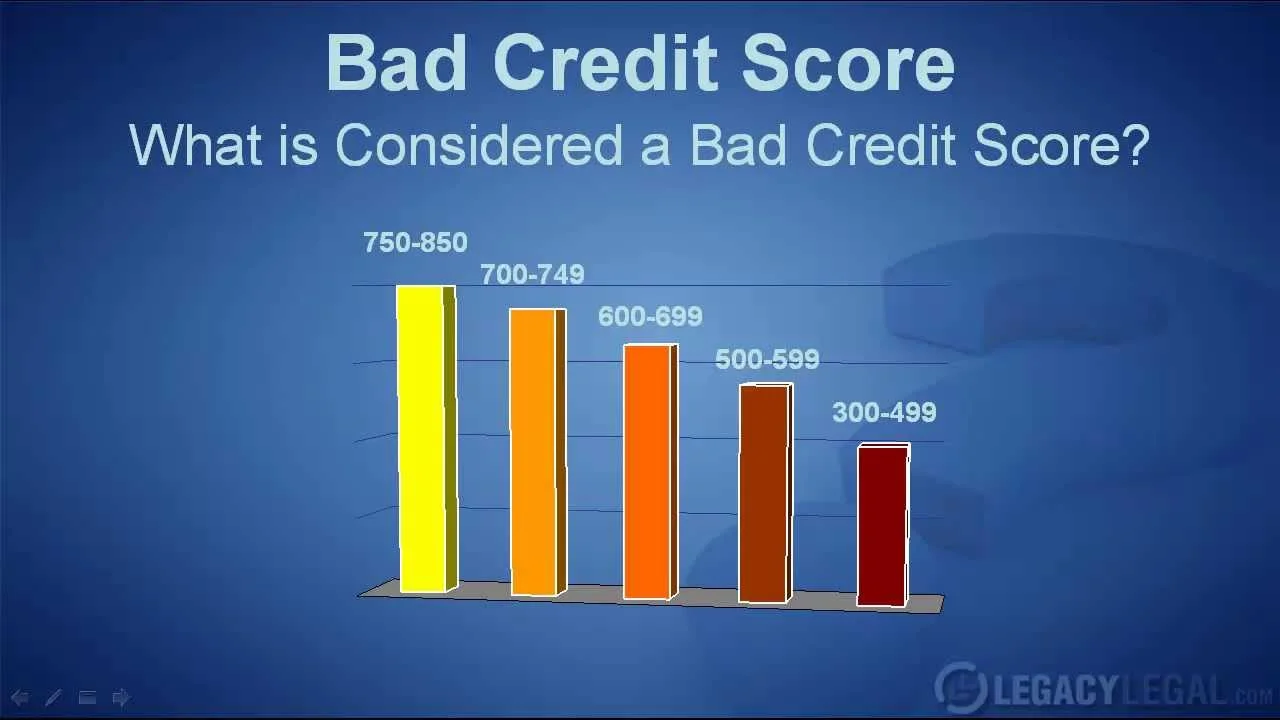

Score Brackets and Their Real Impact on Mortgage Approval

Different ranges of scores give very different results. Here is how each bracket affects mortgage chances in the UAE.

750 to 900 This range is considered excellent. Borrowers in this bracket receive the quickest approvals. Banks offer the best interest rates and the most flexible loans. Down payment requirements often sit at the minimum allowed by regulation.

650 to 749 This range is widespread among UAE residents. Most borrowers here are given conditional approvals. Banks may not offer the lowest down payment requirements and may apply average interest rates. Sometimes the lender asks for additional documents, such as salary letters or bank statements for more years.

550 to 649 This range causes the banks to be cautious. Lenders look closely at every case to understand the reasons for the lower score. Loan amounts may be reduced. Interest rates may increase. Some banks may outright refuse the application.

300 to 549 This range is in the high-risk category. Most lenders deny mortgage applications from borrowers falling in this bracket. Even if the applicant is a high earner, the score indicates repeated problems with repayment behaviour.

Two people with the same score are still able to get different lending decisions because banks also analyse credit mix, the stability of employment and the overall financial behaviour. For example, a borrower with a score of 680 and a stable five-year employment history may be perceived as safer than someone who has a score of 680 but has a short work history.

What Mortgage Lenders Look At Other Than Your Score?

Banks in the UAE have a holistic view of every application. A strong credit score helps, but there are a number of other factors in determining approval.

Debt Burden Ratio DBR is a measure of all monthly debt payments relative to monthly income. UAE Central Bank regulations cap DBR at a maximum of 50 per cent. If your DBR is already high, banks cannot legally approve a mortgage, no matter your credit score.

Length of Credit History Longer credit histories give banks more confidence, as they show long-term repayment behaviour. New expats may find it difficult because their UAE credit history is brief.

Type of Existing Debts Credit cards with high usage, personal loans with long tenures or auto loans with high instalments all factor into the approval. Some types of debt are more worrying to lenders than others.

Payment Quality Borrowers who consistently pay only the minimum amount due on credit cards at times look risky. Banks prefer borrowers who pay full or high percentages of their balances.

Employer and Job Stability The employed category, the duration of employment and the contract type are taken into consideration by the lenders. Stable employment leads to better chances of approval.

Residency Status Resident expats can typically access 75–80% LTV with at least six months of local employment, while non-residents qualify only for ready freehold properties at 50–60% LTV. Expat and national borrowers face different lending criteria.

Bank Account Behaviour Banks also observe patterns of incoming salaries, average balances and sudden large withdrawals. Consistent behaviour is trustworthy.

How Credit Score Affects Mortgage Interest Rate In the UAE?

A high score means that you have more loan products to choose from. Banks compete for low-risk clients because these clients are less likely to go into default. The lower the risk, the lower the price. Borrowers who have excellent scores sometimes enjoy some of the best mortgage rates available.

A lower score can boost interest rates through risk-based pricing. The lender determines a rate that is commensurate with the level of risk for the borrower. This rate may be noticeably higher for someone with a 620 score than a 760 score. In 2026, navigating the UAE mortgage landscape requires knowledge, planning and strategic decision-making — with competitive interest rates and digital platforms making it more important than ever to enter the process with a strong credit profile.

Although the numbers differ by bank, the trend is the same. A high score implies greater negotiating power. A lower score means limited offers and higher costs.

Credit Score Requirements for Different Mortgage Types

Different categories of mortgages have slightly different expectations. Here is what buyers need to know.

First Time Homebuyer Mortgage Banks seek stable income and a score of more than 650. Borrowers who have better scores receive better offers.

Second Home or Investment Mortgage These loans are riskier because the borrowers already have one mortgage. Banks typically prefer scores above 700.

Off-Plan Mortgage Financing Developers and banks expect clean credit histories. High scores help get better terms, especially for financing after construction starts.

Buyout Mortgage When switching banks, your new bank looks at your recent credit behaviour. A good score helps secure a better rate than your existing loan.

Non-Resident Mortgages Some banks may set higher requirements for non-residents — typically 700 or above — as these cases are considered higher risk. Lenders consider non-resident applications with greater scrutiny.

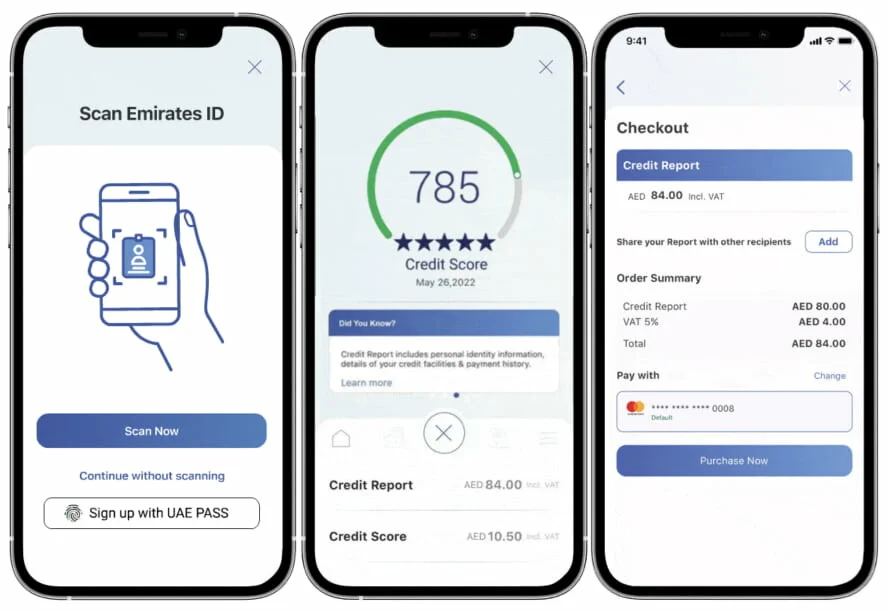

How To Check Your UAE Credit Score? (Simple, Updated Guide)

There are three basic types of reports provided by AECB:

- ● Credit score only

- ● Credit report only

- ● Combined score and report

You can get them from the AECB mobile app, the official AECB website, the DubaiNow app or service centres all over the country. The process is simple — select the report, authenticate your identity and make payment. Payment history is the most important parameter for your AECB credit score, weighing up to 35% of your total score.

Checking your score does not lower your score. Buyers who are thinking of buying a property should check their score at least three to six months before applying for a mortgage. This provides enough time to resolve any problems.

Common Reasons for Low Credit Scores in the UAE

There are a number of issues that will cause your score to be lower. Understanding them helps you to avoid mistakes.

- ● High Credit Card Utilisation — Charging most of your credit limit is a sign of risk. Even if you pay on time, high utilisation hurts your score

- ● Missed or Late Payments — One late payment can set your score way back. Repeated delays result in more damage

- ● Too Many Credit Enquiries — Applying for multiple cards or loans in a short period signals financial stress

- ● Unpaid Telecom Bills — Telecom companies in the UAE report unpaid amounts to AECB. Even a small outstanding bill impacts your score

- ● Bounced Cheques — Cheque returns are tracked by banks and AECB. A bounced cheque is a severe negative mark

- ● Dormant Credit Lines — Old open credit facilities that you no longer use are still counted in your profile

- ● Lack of Credit Mix — Not having a variety of credit types can also negatively affect your score, as lenders want to see your ability to manage different forms of credit responsibly

- ● Short Credit History — New expats usually begin with lower scores, as the system doesn't have much data on them

How To Improve Your UAE Credit Score Before Applying for a Mortgage

Improving your score takes time, but the results make a big difference. Here are practical steps:

- ● Keep credit card utilisation below 30 per cent

- ● Pay all outstanding dues on time for a minimum of three to six months

- ● Clear up telecom and bank charges immediately

- ● Don't apply for new credit cards and loans

- ● Consolidate debts if you are struggling to make the instalments

- ● Request a higher credit limit to improve your utilisation ratio

- ● Maintain a healthy mix of credit types where possible

- ● Review your report on a regular basis and dispute errors if you find any — AECB's website has a dedicated data correction tool for this purpose

Consistency produces more impact than one-off solutions. Even small improvements help to strengthen your mortgage application in Dubai.

Mistakes Purchasers Make when Applying for a Mortgage With a Low Score

Borrowers with lower scores sometimes try to get around the system, but they often create bigger problems.

Common mistakes include:

- ● Making multiple applications to multiple banks — each inquiry reduces the score

- ● Hiding existing liabilities — banks can see everything through AECB, so hiding debt leads to instant declines

- ● Applying without pre-approval — this carries a higher risk of rejection

- ● Choosing a bank that does not match their credit profile — some lenders are strict, while others are more flexible

- ● Closing old credit card accounts thinking it will help — it can actually take at least six months for a closure to reflect, and removing a long-standing account may shorten your credit history and lower your score

Being strategic is a way to protect your score and increase the chances of approval.

Real Examples: How Credit Score Impacted Mortgage Results?

Here are some simple examples based on actual patterns observed in the UAE.

Example One A borrower with a 720 score applied for a mortgage. The bank offered a lower interest rate, as the applicant had good repayment behaviour. Over 25 years, this equated to significant savings in interest compared to a person with an average score.

Example Two Another applicant with a 580 score was rejected by two banks because of repeated late payments. The person then cleared outstanding dues and paid all credit card bills on time for six months. The score increased, and the third application was approved with a higher down payment.

Example Three A non-resident buyer had great credit overseas but a low UAE score since they had no local credit history. The bank asked for additional documents and lowered the loan amount. After opening a small credit card and maintaining good behaviour for a few months, their UAE score improved and new offers became available.

Does a Low Credit Score Mean You Cannot Buy Property In The UAE?

A poor score makes it more difficult, but not impossible, to be approved for a mortgage. Buyers do not have to give up.

Higher Down Payment — Some banks will approve lower score profiles provided the borrower makes a bigger down payment.

Private Mortgage Lenders — There are private lenders that will take cases traditional banks won't. Terms may be more expensive but still workable.

Developer Payment Plans — Off-plan properties are often available with flexible payment plans and no mortgage checks.

Rent-to-Own Schemes — This option allows buyers to move into the home first and convert payments into home ownership at a later time.

Real Estate Agency Support — Experienced agencies help to structure deals that fit the buyer's profile.

Mortgage Approval Checklist for UAE Buyers

This simple checklist helps you prepare:

- ● Check your credit score

- ● Review your DBR

- ● Organise salary letters, IDs, and employment documents

- ● Prepare bank statements

- ● Keep your down payment ready

- ● Avoid new debts before applying

- ● Apply only through pre-approved channels

How a Real Estate Broker Helps You Navigate Mortgage Approvals?

A skilled broker reduces stress and speeds up the process. Here is how they support buyers:

- ● Study your credit report before applying

- ● Compare banks and find the one matching your score

- ● Connect you with mortgage advisors

- ● Recommend properties that suit your lending capacity

- ● Prevent repeated rejections that could harm your score

FP Property guides buyers through every step — including pre-assessment, document review, bank selection, and negotiation support.

Conclusion: Strengthening Your Credit Score Before Buying Property in the UAE

Your credit score is one of the most important factors in securing a mortgage in the UAE. A strong score gives you better rates, faster approval, and higher loan amounts. If you are planning to buy property in Dubai in 2026, starting your mortgage process early will help you secure better rates and smoother approval. Checking your score early helps avoid problems later. With careful planning and professional support, you can improve your chances and choose the right property confidently.

For personalised guidance, FP Property offers detailed mortgage support in the UAE tailored to your financial profile.